The global metals and mining industry posted one of its strongest financial performances in two decades last year, earning $700 billion in profits despite a 6% drop in revenue, according to McKinsey’s newly released Global Materials Perspective 2025.

The report highlights that while profitability remains robust, the sector faces mounting challenges from declining ore grades, complex mining conditions, and stricter environmental and labour standards. All of these factors are driving up costs and squeezing margins, McKinsey said, noting that sustained investment in technology, electrification and digital tools will be crucial to maintaining productivity gains.

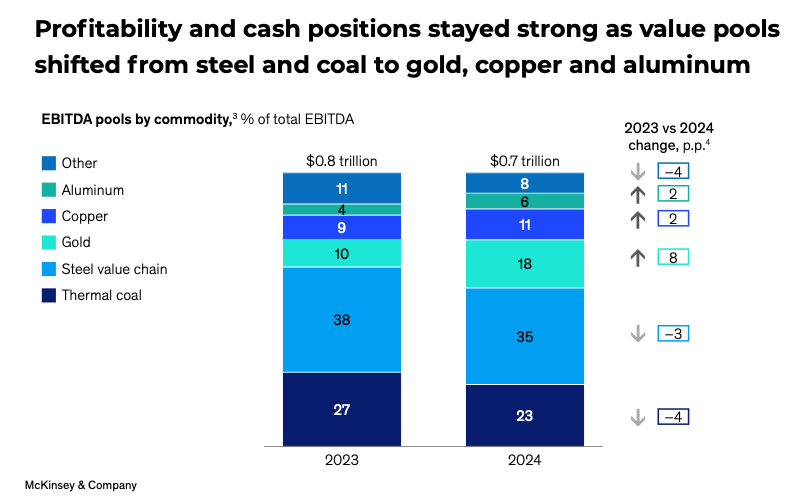

Profit pools have shifted from coal and steel toward copper, gold, and aluminium, as productivity has rebounded by roughly 1% annually since 2018, led by Latin America and North America. The industry’s structure continues to fragment: the market share of the top 10 mining firms has fallen from 60% in 2000 to 30% in 2015, where it has since stabilized.

Regional shifts are reshaping the sector. China and North America have gained share, while Europe’s dropped to 11%. Steel’s share of total market value has halved since 2000, now standing at 10%. Demand remains resilient, with more than half of forecasted growth through 2035 expected to come from energy transition materials. McKinsey notes that artificial intelligence (AI) data centres alone could drive a 3% increase in global copper demand by 2030, underscoring technology’s growing influence on raw material markets.

Asian lead

Asian nations are projected to dominate demand growth, accounting for more than 45% of global expansion by 2035. Meeting this demand will require $4.7 trillion in capital investment, 270 GW of new power capacity, and 350,000 new jobs worldwide. Despite pressures, capital markets remain strong, with total shareholder returns up 3.5 times and market capitalization doubling since 2015.

The report identifies four key shifts since last year’s edition: rising resource nationalism; accelerated materials demand from AI technologies; a visible rebound in productivity driven by generative AI and automation; and slowing decarbonization. This is particularly true in Europe’s steel industry, where nearly one-third of planned projects have been delayed or cancelled.

Coal’s around

Thermal coal production, meanwhile, reached a record eight gigatons, signalling uneven progress on the energy transition. Still, the long-term demand outlook remains positive, fuelled by population growth, expanding middle classes, and the adoption of low-carbon technologies.

McKinsey outlines three strategic opportunities for industry leaders: expanding into new geographies and critical materials, leveraging AI and automation to sustain productivity, and pursuing pragmatic, cost-effective decarbonization. With 30–50% of shareholder overperformance driven by operational decisions, disciplined growth and innovation will be key to enduring success.

“Success in metals and mining will hinge on improving productivity and delivering sustainable solutions,” the report concludes. “Those willing to act decisively will be best positioned to seize the opportunities ahead.”

Global miners raked in $700B in 2024 despite rising pressures